On April 23, 2026, Lucid Group's stock dropped

10% in a single session. No earnings miss. No recall announcement. No executive departure. The drop came on a single rumor: that Saudi Arabia's Public Investment Fund, which owns 57% of Lucid and has poured more than $8 billion into the company since 2018, was considering taking the company private.

The market's reaction told you everything you need to know about what LCID is today. The stock did not drop because the take-private rumor was bad news. It dropped because investors realized that the only clean exit for Lucid might be one where public shareholders have no leverage at all.

Six weeks earlier, on February 20, Lucid had laid off 800 people — 12% of its workforce, the third round of cuts since 2023. Five days after that, it reported Q4 2025 earnings: revenue of $522.7 million, up 123% year over year, which sounds transformative until you see the cost of revenue was $944 million. For every dollar Lucid earned selling cars, it spent nearly two dollars building them. The gross margin: –75.2%.

On April 14, two things happened simultaneously. First, Lucid named Silvio Napoli, the chairman and CEO of Schindler Group, the Swiss elevator and escalator giant, as its next permanent CEO. Second, it announced a $1.05 billion capital raise — $550 million in convertible preferred stock from the PIF, $300 million from a registered public offering, and $200 million from Uber, which expanded its total investment to half a billion dollars.

Then on May 5, Lucid reported Q1 2026: revenue of $282.5 million against a $358.5 million consensus, a net loss of $1.02 billion, a gross margin of –110.4%, and — the line that moved the stock to within a dollar of its all-time low — the suspension of its 2026 production guidance pending Napoli's strategic review.

Today, May 26, 2026, LCID trades at $5.84. It is 83% below its 52-week high of $33.70.

I'm telling you this because Lucid is not a consumer turnaround in the way Peloton or Lululemon is. It is not a brand that overexpanded and needs to find its customers again. It is a pre-profitability industrial company with world-class EV technology, sovereign-backed capital, a robotaxi partnership that just received California DMV driverless approval, and a cost structure that will kill it before any of those advantages matter — unless the new CEO can bend the margin curve fast enough.

The two Lucids are not separated by customer sentiment or employee morale. They are separated by time. The question is whether the cash lasts long enough for the business to arrive.

Investment Council: $LCID: AVOID (MEDIUM conviction) → | All current verdicts: The Verdict Board →

undefined

How Lucid got to $5.84

The decline is older than the recent earnings miss.

Lucid went public via SPAC in July 2021 at an implied valuation of $24 billion. The thesis was elegant: Peter Rawlinson, former chief engineer of the Tesla Model S, had built a better electric sedan. The Lucid Air won MotorTrend Car of the Year. The 520-mile EPA range was the longest of any production EV. Saudi Arabia's PIF had been backing the company since 2018, and the factory in Casa Grande, Arizona was scaling toward 34,000 units per year.

Then the scaling didn't happen. In 2022 Lucid delivered 4,369 vehicles against an original 20,000-unit target. In 2023 it delivered 6,001 against a 10,000-unit guide. In 2024 the number climbed to 10,241, still roughly half the factory's theoretical throughput. The problem was never demand — it was production yield, supply chain execution, and the brutal unit economics of building a $70,000+ sedan at low volumes.

By Q4 2024, the market had re-priced LCID from a Tesla challenger to a cash-burn machine. The stock was below $3. Then something shifted.

In late 2024, Lucid launched the Gravity SUV. It was named the 2026 World Luxury Car of the Year. It opened the addressable market from sedans to the vastly larger SUV segment. Q4 2025 production surged to 9,029 units and deliveries hit 10,241, more than all of calendar 2023 in a single quarter. Revenue nearly tripled quarter over quarter.

The stock rallied from $3 to $33.70. Then it gave it all back.

The Q1 2026 collapse had three overlapping causes. First, a supplier quality issue with second-row seats forced a 29-day production halt for the Gravity, and a recall of 4,476 vehicles. Second, a separate recall hit 3,627 Air sedans for a half-shaft bolt defect that had first surfaced in October 2025. Third, Peter Rawlinson stepped down as CEO in February 2025, Marc Winterhoff served as interim for over a year, and the permanent replacement didn't arrive until April 2026. Leadership continuity evaporated at the exact moment the production ramp needed it most.

That is how Lucid got to $5.84.

undefined

What the financials show

The income statement is a contradiction. Revenue is growing and the company is losing more money.

Metric | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 | Q1 2026 |

|---|---|---|---|---|---|

Revenue ($M) | 235.0 | 259.4 | 200.0 | 522.7 | 282.5 |

Revenue YoY | +36% | +33% | — | +123% | +20% |

Gross margin | –171.3% | –117.0% | –140.0% | –75.2% | –110.4% |

Deliveries | 3,109 | 2,394 | 2,781 | 10,241 | 3,093 |

Production | 2,212 | 2,551 | 3,158 | 9,029 | 5,500 |

Net loss ($B) | –0.65 | — | — | — | –1.02 |

Total liquidity ($B) | 5.0 | — | — | 4.6 | 3.2* |

*Post-Q1 liquidity was approximately $3.2B, boosted to approximately $4.25B following the April 2026 capital raise.

The critical number is not revenue. It is gross margin. At –110.4% in Q1 2026, Lucid spends $2.10 to manufacture each dollar of revenue it earns. The Q4 2025 print of –75.2% was the best quarter in recent history, driven by Gravity volume before the supplier halt derailed the ramp. The linear trend across the last five quarters shows improvement of 16.4 percentage points per quarter, but the R-squared is 0.52 and the p-value is 0.17 — the improvement is visible but not yet statistically significant.

At the linear trend rate, Lucid reaches gross margin breakeven around Q2 2027. At the current burn rate of approximately $850 million to $950 million per quarter, the $4.25 billion post-raise liquidity lasts four to five quarters — until roughly Q2 or Q3 2027.

That is the central tension. The cash runway and the margin convergence point arrive in the same neighborhood. If the margin improves faster than the linear trend (because Gravity volume ramps and fixed costs spread), the company survives to fight for profitability. If it doesn't, there is another capital raise, another dilution event, and another leg down for the stock.

Full-year 2025 results: revenue $1.35 billion (up 68% year over year), net loss per share of –$5.50 (improved from –$12.52 in FY2024), total accumulated losses since founding of $14.8 billion.

The company suspended its 2026 production guidance of 25,000 to 27,000 vehicles pending new CEO Napoli's strategic review. Winterhoff said on the Q1 call that he expects deliveries to be back-end-weighted for the year, but no specific numbers were given. The updated outlook will come at Q2 earnings in August.

undefined

Methodology and sample sizes

Lucid is not a consumer brand in the way that Peloton or Lululemon is. It does not have millions of monthly active subscribers writing Reddit posts about their morning rides. It sells approximately 10,000 to 15,000 luxury vehicles per year to a niche buyer base. The consumer-voice channels that anchor most Turnaround Radar reports — Trustpilot, BBB, App Store reviews — are either extremely thin or nonexistent for Lucid.

This report pivots accordingly, toward (a) financial-disclosure analysis, (b) social-media-momentum analysis, and (c) employee sentiment, while being transparent about what is thin.

Channel | Sample size | Time window | What we looked for |

|---|---|---|---|

Financial disclosures | 5 quarterly earnings + 4 8-K reports | Q1 2025 – Q1 2026 | Revenue, margin trajectory, cash burn, delivery cadence |

SEC filings | 10-Q, 10-K, 8-Ks | FY2025 – Q1 2026 | PIF ownership, capital raise terms, going concern language |

Analyst consensus | 6–19 analysts | May 2026 | Price targets, rating distribution |

~40 posts/threads | Jan – May 2026 | Gravity quality complaints, Nuro/Uber reception | |

Stocktwits | Sentiment index | May 2026 | Retail trader sentiment direction |

Glassdoor | 1,232 reviews | Last 12 months | Rating, CEO approval, business outlook |

Indeed | 197 reviews | Recent | Job security, management quality |

Trustpilot | 12 reviews | Lifetime | Extremely thin — not statistically usable |

BBB | No profile found | — | Channel does not apply |

NHTSA recalls | 4 recall campaigns | 2025–2026 | Gravity seatbelts, Air half-shafts, software, airbags |

What is missing and why it matters: The consumer-voice data that powered the PTON and LULU reports — thousands of dated, time-sliceable reviews across multiple platforms — does not exist for LCID. Trustpilot has 12 reviews total. BBB has no profile for the EV company. There is no mass-market app with App Store reviews. The absence of consumer-voice data is itself a signal: Lucid's customer base is too small and too niche for the review platforms that capture mass-market sentiment. This limits our ability to run the same powered statistical tests we ran on Peloton. We are transparent about this constraint throughout the report.

Statistical test: can Lucid reach gross margin breakeven before the cash runs out?

This is the question the entire thesis hinges on. We cannot run a consumer-sentiment time-series test the way we did for Peloton because the data does not exist in sufficient volume. Instead, we run the test on the financial disclosure data, which is dense, audited, and quarterly.

Dataset: Five quarters of GAAP gross margin from Q1 2025 through Q1 2026.

Test 1 — Linear trend in gross margin.

Quarter | Gross Margin | Revenue ($M) | Deliveries |

|---|---|---|---|

Q1 2025 | –171.3% | 235.0 | 3,109 |

Q2 2025 | –117.0% | 259.4 | 2,394 |

Q3 2025 | –140.0% | 200.0 | 2,781 |

Q4 2025 | –75.2% | 522.7 | 10,241 |

Q1 2026 | –110.4% | 282.5 | 3,093 |

Linear regression: slope = +16.4% per quarter, R² = 0.52, p = 0.17. The trend is directionally positive but not statistically significant at the 5% level. The Q4 2025 data point, driven by the Gravity production surge, pulls the trendline up. The Q1 2026 regression, driven by the 29-day supplier halt, pulls it back down.

Interpretation: The gross margin improvement is real in direction but fragile in magnitude. It depends entirely on sustained Gravity volume. When volume collapsed in Q1 (3,093 deliveries vs 10,241 in Q4), the margin collapsed with it. This is classic fixed-cost leverage in reverse: a factory built for 34,000 units per year running at 12,000 annualized rate cannot amortize its fixed costs.

Test 2 — Delivery trajectory (Mann-Kendall trend).

Kendall's tau = 0.51, p = 0.058. Borderline — the upward trend in deliveries is present but does not clear the 5% significance threshold. The Q4 2025 Gravity surge and Q1 2026 supplier-halt collapse create enormous variance that swamps the signal.

What this means for the trade:

The financial data tells a story of high variance, not of trend. Lucid's best quarter (Q4 2025) was nearly four times its worst recent quarter (Q1 2026) in deliveries. The margin moved 95 percentage points between those two quarters. Until the company strings together two or more consecutive quarters of rising volume without a production disruption, neither the delivery trend nor the margin trend will clear statistical significance. The Q2 and Q3 2026 prints are the test.

undefined

Important caveats

Five data points is a very small sample for regression. The R² of 0.52 means nearly half the variance is unexplained. We report the direction of the trend (improving) with the caveat that it is driven almost entirely by a single high-volume quarter (Q4 2025). Two more quarters of data will tell us whether the trend is real.

The supplier halt in Q1 was a one-time event (Camaco altered its welding process without Lucid's approval). If Q2 and Q3 deliveries return to Q4 2025 levels, the gross margin trend re-establishes on a much firmer base. If they don't, the trend was never there.

Cash burn projections assume the $500 million cost-reduction program (announced Q1 2026, targeting headcount savings over three years) begins delivering savings in H2 2026. If it doesn't, the runway shortens.

What the financials do not show

Three things, and they all live outside the income statement.

The first is what the PIF is actually doing. Saudi Arabia's Public Investment Fund owns 57% of Lucid. It has invested more than $8 billion since 2018. The latest capital infusion in April 2026 — $550 million in convertible preferred stock at 9% annual compounded dividend, convertible at $10.82 per share — carries terms that tell you something important. The conversion price is 85% above the current stock price. The PIF is not converting at $5.84. It is either (a) waiting for the stock to recover above $10.82 before converting, which implies confidence in the long-term thesis, or (b) building a senior claim on the capital structure that positions it for a take-private at a price of its choosing.

The take-private speculation is not fringe. On April 23, the day LCID dropped 10%, Polymarket's "Lucid bankrupt before 2027" contract traded at 51%. The binary framing — take-private or bankruptcy — tells you the market has stopped pricing Lucid as a going concern on the public markets and started pricing it as a PIF option.

The second is the Uber and Nuro robotaxi partnership. In July 2025, Uber, Lucid, and Nuro announced a premium robotaxi program. In April 2026, they expanded it to a minimum of 35,000 Lucid vehicles — Gravity SUVs and midsize platform models — equipped with Nuro's autonomous system, to be deployed exclusively on Uber's platform. On the Q1 call, Winterhoff confirmed that Nuro received California DMV approval for driverless testing of the Lucid Gravity, and the first commercial rides are planned for the San Francisco Bay Area in late 2026.

This is the optionality play that separates Lucid from every other EV startup. Rivian has its own Uber deal (1,000+ R2 vehicles). But Lucid's partnership is larger by an order of magnitude — 35,000 vehicles — and it comes with a built-in revenue stream (Uber invested $500 million and is taking delivery of the vehicles). If the robotaxi unit economics work, Lucid goes from selling 10,000 luxury cars to selling 35,000 fleet vehicles with recurring software revenue. That is a different company at a different valuation.

The third is the midsize platform. Lucid has detailed an upcoming platform with a starting price below $50,000, targeting both fleet and consumer use. The bill of materials is reportedly below initial cost targets. Production ramp is planned for 2027 at the Saudi Arabia AMP-2 facility. This is the volume play: three body styles at half the current price point, built at a factory that sidesteps U.S. tariffs entirely.

None of these three — PIF's strategic intent, robotaxi commercialization timeline, midsize platform unit economics — appear in the Q1 2026 income statement. They are the reason the analyst median price target ranges from $10 to $20 while the stock sits at $5.84. The market is pricing the current income statement. The analysts are pricing the option value.

What is actually happening, and what is not

Recovering:

The delivery ramp, despite the Q1 disruption. Q4 2025 proved the factory can produce 9,000+ units in a quarter when the supply chain holds. Production in Q1 2026 was 5,500 despite the 29-day halt — implying a run rate well above prior quarters when the line was running.

The technology credibility. Gravity won World Luxury Car of the Year. The Air still holds the longest-range production EV crown. Nuro chose the Gravity as the platform for its autonomous system, which is a third-party validation of the vehicle architecture that no marketing budget can buy.

The balance sheet firepower. $4.25 billion in post-raise liquidity. $500 million cost-reduction program. A sovereign wealth fund that has shown willingness to write checks at every stage.

Not recovering:

The unit economics. Negative 110% gross margin. Even the best quarter (Q4 2025 at –75.2%) was disastrously unprofitable by any conventional measure. The path from –75% to 0% requires doubling volume without proportionally increasing variable costs, and Lucid has never sustained that volume for more than one quarter.

Investor confidence. The stock is at $5.84 vs a 52-week high of $33.70. Stocktwits sentiment is bearish. Short interest is 44 million shares, 12% of outstanding. Polymarket prices bankruptcy at 51% before 2027.

Leadership stability. Rawlinson is gone. Winterhoff was interim for over a year. Napoli has been CEO for six weeks and has not yet spoken publicly about his strategic vision — that is coming at Q2 earnings in August. Three leaders in 18 months is not the backdrop for a manufacturing turnaround.

Unknown:

Whether the $500 million cost-reduction program bends the margin curve fast enough. Whether Napoli keeps the current product roadmap or pivots. Whether the PIF exercises the take-private option. Whether the robotaxi program generates meaningful revenue before 2028. These are the questions the next 12 months answer.

Important caveats

This report has significant data limitations compared to our standard methodology. We are transparent about them:

Consumer-voice data is extremely thin. Trustpilot has 12 total reviews. BBB has no profile for Lucid Motors (the EV company). There is no mass-market app store to review. We cannot run the powered statistical tests on customer sentiment that anchored the PTON report.

The gross margin regression has five data points. R² = 0.52, p = 0.17. This does not pass the 5% significance threshold. We report the direction of the trend (improving) with the caveat that it is driven almost entirely by a single high-volume quarter.

Delivery trajectory is borderline significant. Mann-Kendall tau = 0.51, p = 0.058. The Q4 2025 spike and Q1 2026 collapse create enormous variance.

Employee data (Glassdoor 3.3/5, 1,232 reviews) is usable but not time-sliceable. The 9% year-over-year improvement in the overall rating is directionally positive but we cannot slice it into monthly bins for a time-series test.

PIF's intentions are unobservable. The take-private scenario (which we assign 20% probability) is based on market speculation and economic logic — not on any disclosed filing or statement.

The setup

Three things frame the trade beyond the fundamentals.

Short interest is 44.08 million shares, approximately 12% of outstanding. That is lower than Peloton's 18% but still meaningful — enough that a genuine positive surprise (Q2 earnings beat, take-private offer, or Nuro commercial launch) creates mechanical covering pressure.

The PIF's position creates a structural floor. Saudi Arabia has invested $8 billion in Lucid. At the current market cap of roughly $14 billion, the PIF's 57% stake is worth approximately $8 billion — roughly its cumulative investment at cost. A take-private at $7.50 to $9.00 per share would allow the PIF to consolidate ownership at a price modestly above its effective cost basis while eliminating the quarterly scrutiny of public markets. The economics favor going private.

The new CEO is an operational turnaround specialist, not a visionary founder. Silvio Napoli ran Schindler, a $15 billion industrial conglomerate, and is known for cost discipline and manufacturing efficiency. That is exactly what a –110% gross margin company needs. It is not what a "move fast and break things" technology startup needs. Which version of Lucid Napoli chooses to build is the single most important question for the stock in the next 12 months.

undefined

The trade

Most EV stock analysis is one-axis. Retail investors read the technology specs. Reddit reads the delivery numbers. Wall Street reads the cash burn. Saudi Arabia reads the geopolitics. In a real turnaround, all four converge. In a forced exit, they do not.

Lucid today has convergence on exactly one axis: technology. The Gravity is a world-class vehicle. The powertrain is best-in-class. The Nuro partnership validates the autonomous-ready architecture. None of the other three axes — manufacturing economics, investor sentiment, leadership stability — have converged yet. The trade is whether they start converging before the cash runs out.

Run the cash math forward and the picture sharpens.

At the current burn rate of approximately $900 million per quarter, the $4.25 billion post-raise liquidity lasts until roughly Q2 2027. The cost-reduction program targets $500 million in savings over three years, implying perhaps $80 to $100 million in quarterly savings by mid-2027 — meaningful but not transformative. Unless Gravity volume returns to Q4 2025 levels and stays there, there is another capital raise in 2027. The terms of that raise — equity at $5, or convertible preferred at $10, or PIF take-private at $8 — determine whether current shareholders participate in the upside or get diluted out of it.

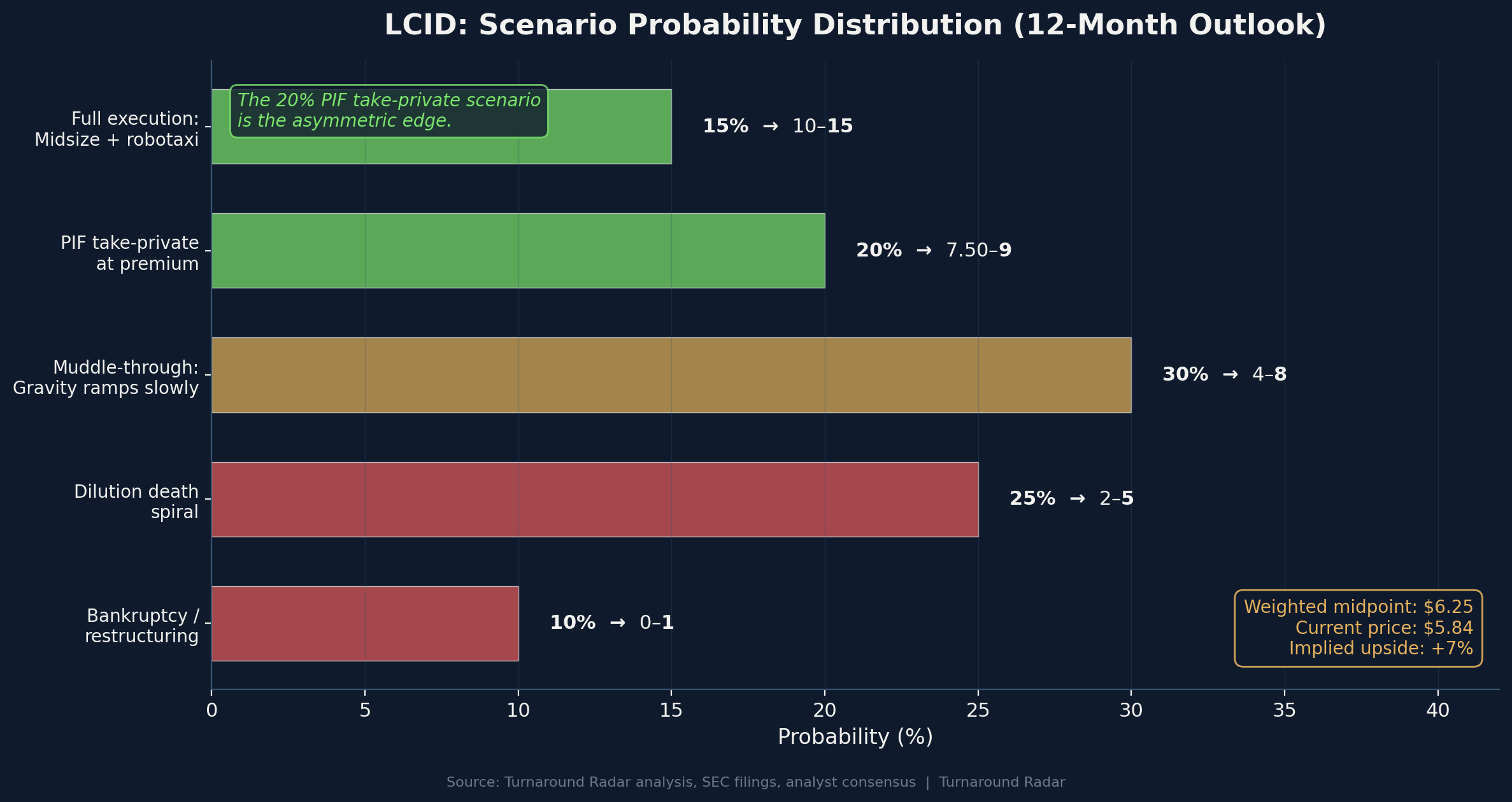

I put the probability distribution across five scenarios:

Scenario | Probability | 12-Month Price Range |

|---|---|---|

PIF take-private at 30–50% premium | 20% | $7.50 – $9.00 |

Full execution (Midsize + robotaxi catalyze rerating) | 15% | $10.00 – $15.00 |

Muddle-through (Gravity ramps slowly, cash lasts to 2028) | 30% | $4.00 – $8.00 |

Dilution death spiral (more raises at depressed prices) | 25% | $2.00 – $5.00 |

Bankruptcy or restructuring | 10% | $0.00 – $1.00 |

Weighted 12-month midpoint: $6.25 vs current $5.84. Implied upside: +7%.

That 7% weighted return does not scream conviction. The asymmetry is in the tails. The 20% take-private scenario returns 28–54%. The 15% full-execution scenario returns 71–157%. Combined, there is a 35% chance of significant upside. But there is also a 35% combined probability of dilution death spiral or bankruptcy, which returns –14% to –100%.

The trade that falls out of this is a gated entry, not a starter position:

Now ($5.84). No position. The weighted expected return of +7% does not compensate for the binary risk. Unlike PTON at $5.71, where the cash floor was $1.13 billion and free cash flow was positive, Lucid is burning $900 million per quarter with negative gross margin. There is no cash floor here — there is a cash countdown.

August 2026 (Q2 earnings + Napoli's strategic review). This is the first real entry gate. If Napoli reinstates production guidance above 20,000 units, if Q2 deliveries show a recovery toward Q4 2025 levels, and if the gross margin improves sequentially to better than –80%, consider a small tracking position at 0.5% to 1% of portfolio. The Napoli print is the single most important data point between now and year-end.

Late 2026 (Nuro commercial launch in SF). If robotaxis are carrying passengers on Uber by December, the optionality re-prices. The 35,000-vehicle commitment becomes a revenue pipeline, not a press release. Add to 1% to 2% of portfolio if the pilot launches on time.

2027 (Midsize production + next capital event). If the midsize platform enters production and the unit economics are materially better than Gravity (BOM below targets suggests they could be), size to 2% to 3%. If instead there is another dilutive raise below $5, exit entirely.

PIF take-private offer. If it comes, the offer price is the trade. At $7.50 to $9.00 (our range), you need to own shares before the announcement. The gated-entry approach above puts you in position if the August and December gates clear. If the take-private comes before August, you miss it — and that is fine. The 20% probability of that scenario does not justify holding a –110% gross margin company at a 7% weighted expected return.

There is no "buy now and hold for the robotaxi future" trade in LCID at $5.84. There is a "wait for the new CEO to show you his hand, then decide" trade. The asymmetry only pays if you let the company show you the answer instead of trying to guess it in May.

The August read

The two Lucids do not merge on a single date. But the date they are scheduled to start merging is August 2026 — when Lucid reports Q2 earnings and Silvio Napoli delivers his first strategic update as CEO.

Within 24 hours of that print, Turnaround Radar subscribers get the follow-up: Did Napoli reinstate guidance? What did Q2 deliveries look like? Did gross margin improve? Is the take-private still on the table? Am I opening a tracking position, or staying on the sideline?

Same drill in late 2026 when the Nuro robotaxi pilot launches. Same drill in 2027 when the midsize platform enters production. Every catalyst on the ladder gets its own update, on the day it resolves, with the specific sizing call attached.

If you want the August read in your inbox the morning it lands, subscribe below. The setup we've laid out only pays if you act on the right catalyst — and the right catalyst is the one with a date attached.

Investment Council: $LCID: AVOID (MEDIUM conviction) → | All current verdicts: The Verdict Board →

Turnaround Radar covers consumer brand and growth stocks trading 30%+ below their 52-week highs, distinguishing real recoveries from value traps. Next report: Roblox (RBLX).

This is research, not investment advice. The author does not own LCID at time of publication.